How to invest to buy cars

The smart way to buy and replace cars over your lifetime without having a car loan.

Australian’s are driving around in debt.

Australians love their cars, and it shows. We have one of the highest new-car uptake rates in the world. The shift toward electric and hybrid models is also accelerating new car purchases with higher price tags. In the first half of 2025, hybrid sales increased by 51.5% and plug-in hybrids rose by 88.5%.

While the demand for new cars grows, so does the price and debt behind each purchase.

$4.9 billion of new car loans were issued in the June 2025 quarter (ABS), with the average car loan now topping $33,000.

Relentless marketing tells us to upgrade our cars every few years using debt. ‘Easy credit’ is designed specifically to sell more vehicles - no matter the true driveway cost.

But there’s a better way to buy and replace cars…

Let’s explore:

What is the real cost to buy a car?

Most Australians purchase cars through one of two ways: saving cash, or getting finance through either a car loan or their home loan.

But there’s a third way… Investing to buy.

Imagine that you own your current car and you’re planning to replace it in 7 years time.

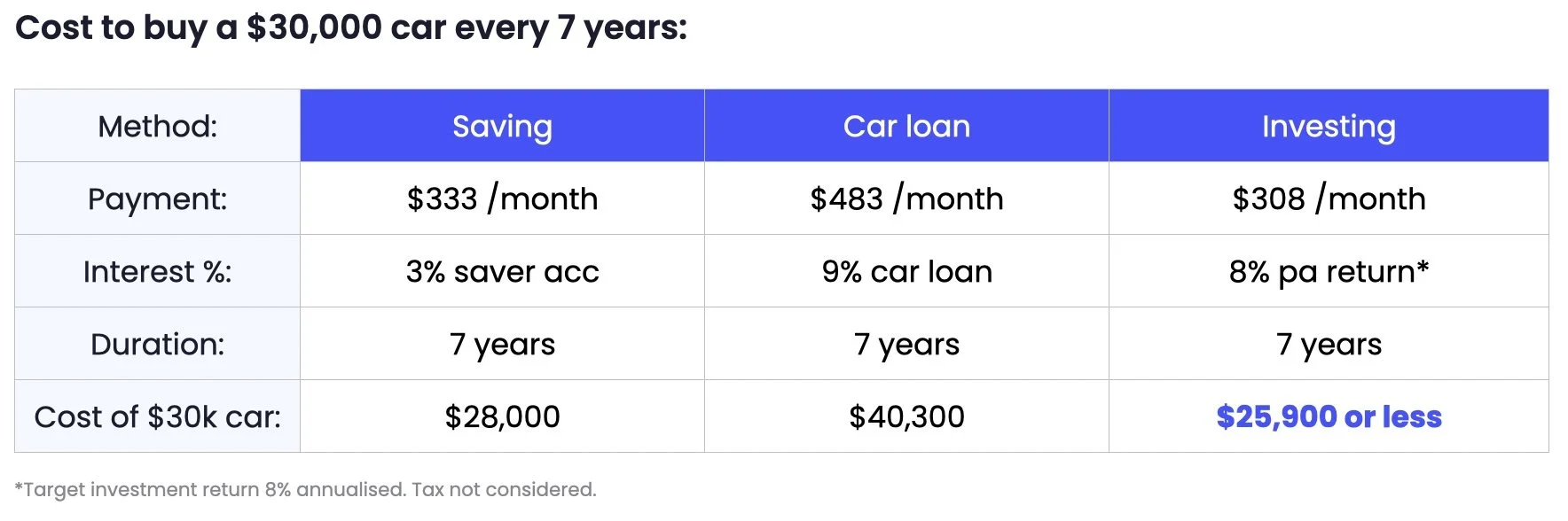

The table below compares the different ways of purchasing a $30,000 car over a 7 year period, which is the average time before a car is considered to be replaced.

Saving to buy: If you save ~$330 per month in a savings account with 3% interest, in approximately 6 years and 10 months you should have $30k saved, with a small help from the interest earned.

Car loan or home loan: If you take out finance, you can expect to pay between 6 and 12% interest on your loan. Your total cost to buy a $30,000 car will be well over $40,000, not including typical loan fees such as: account keeping fees, loan establishment fees, early repayment fees, or a balloon fee at the end.

If you draw money out of your home loan, while you may be paying a lower interest rate compared to a car loan, you are breaking momentum in owning your home. The longer you take to repay the principal debt on your home loan balance, the more money in interest you will have to take from your family to give to your lender. It’s a race against time, and buying cars using your home loan will only slow you down.

Investing to buy: If you allocate money each month to create financial assets, those assets can produce an income (and grow in value) that compounds over time and generates more income for you. This means the cost to buy a $30,000 car can be significantly lower, and continue to be lower the longer you stay investing.

“Instead of working for the bank’s profit, put your own money to work”

Using debt -vs- investing to create income assets

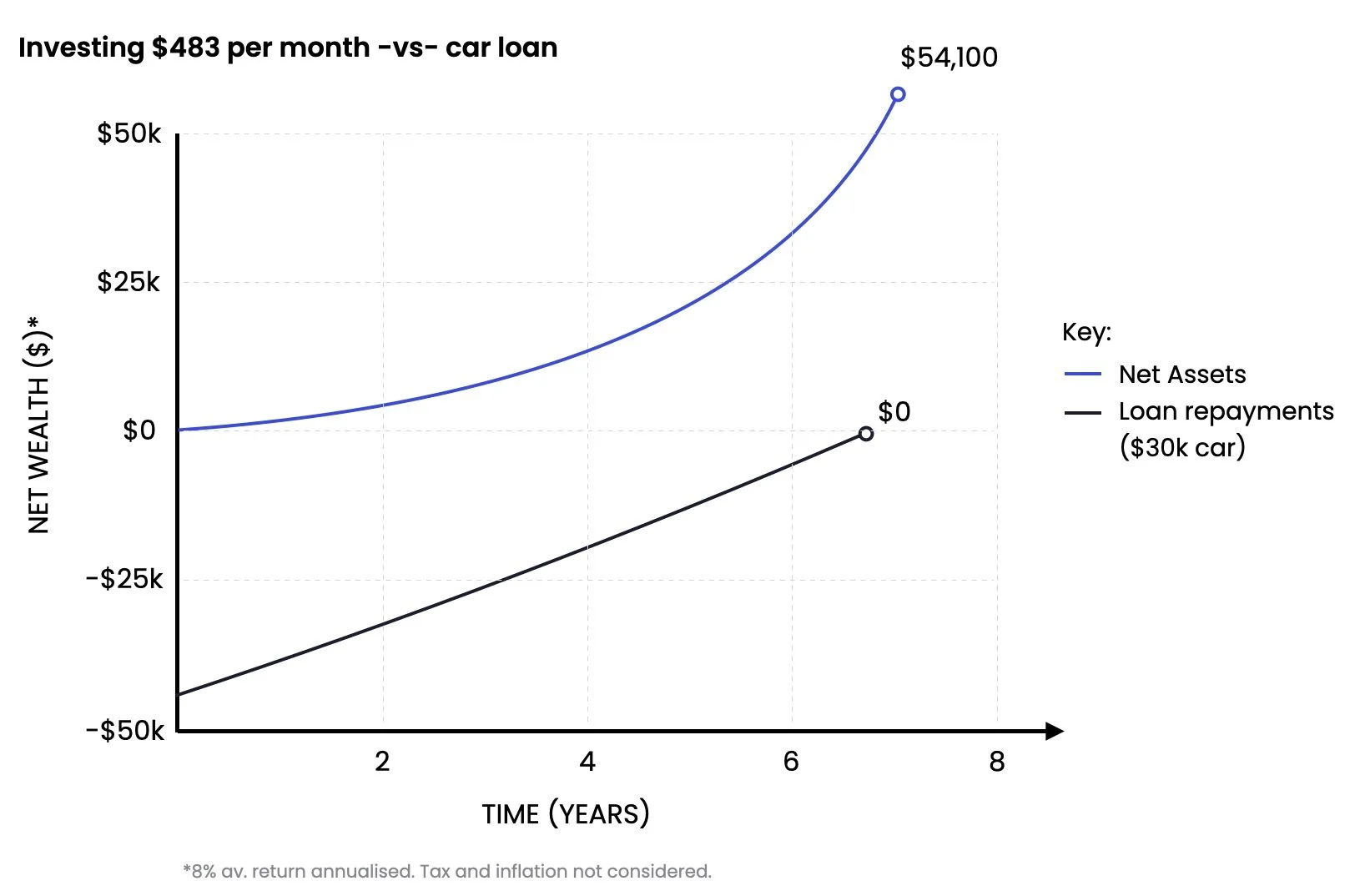

Instead of taking out a car loan, what could you achieve if you purchased income and growth assets with the average loan payments of $483 per month, over the same period…

The graph above shows your assets over a 7 year period. If you get a car loan, you’ve achieved nothing, except overpay for a car that now needs to be replaced.

But if you’ve invested $483 per month, assuming an 8%pa return, you could have over $54,000 — ready to purchase a car with money left over to keep growing your investment.

The ‘Million Dollar Car’ strategy

If you look beyond 7 years, this investment strategy continued will compound to generate more money, the longer you continue building your financial assets.

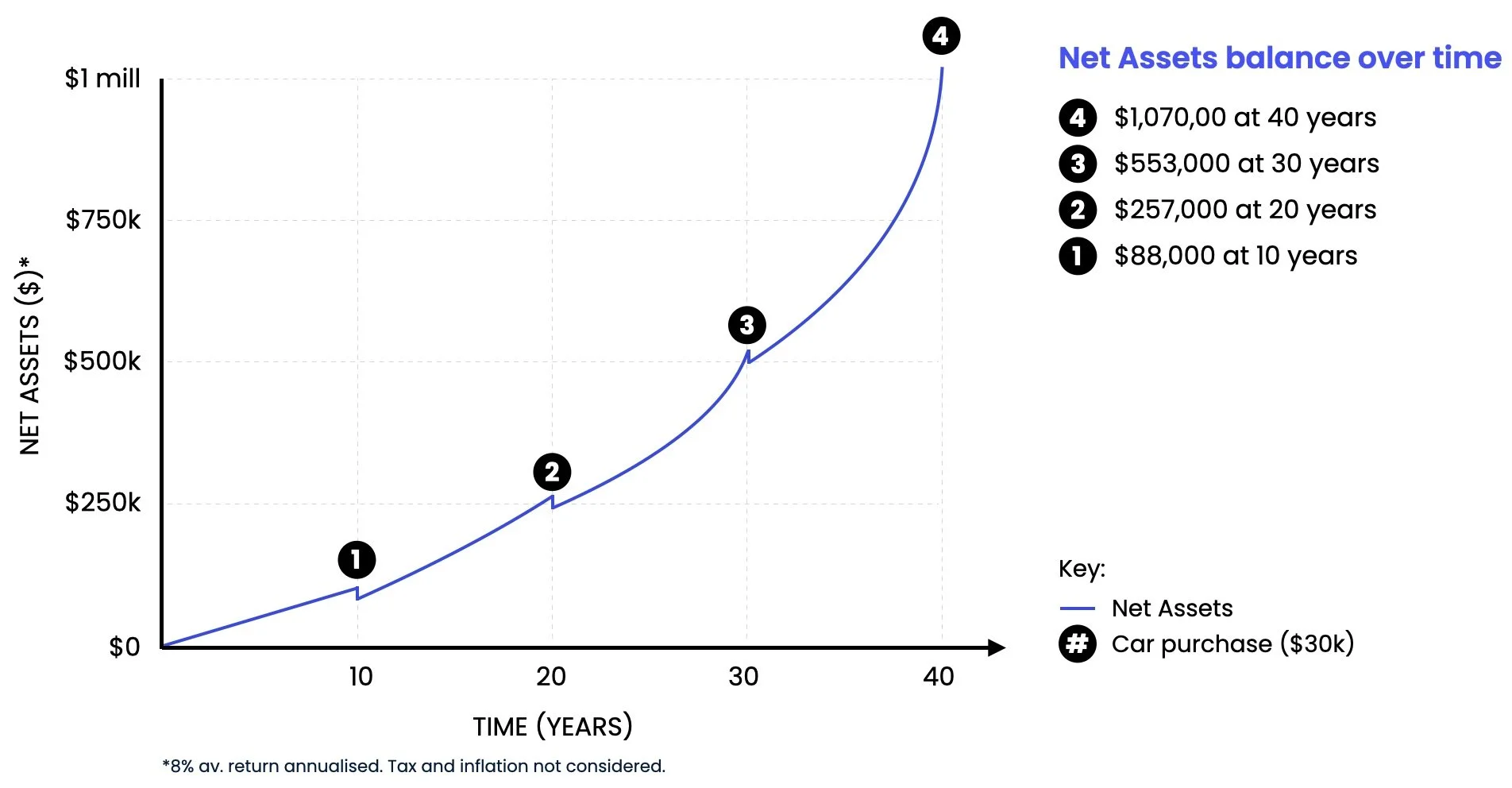

Instead of making the lenders wealthier, let’s see what could happen if you continue to invest ~$483 per month over your working life:

The graph above shows a growing investment balance, with withdrawals for 4 car purchases (of $30,000) every 10 years, over 40 years.

At the end of 40 years, you have purchased your 4th car, using funds from your investments, and your investment assets are over $1 million dollars. Assumptions apply.

That’s the power of compounding growth.

Notice how much your investments grow in the final 10 years, compared to the first period.

“Compound interest is the 8th wonder of the world. He who understands it, earns it; he who doesn’t, pays for it”

The mindset shift

When you ditch debt and invest, you have options. You can negotiate car prices, you can change cars more often without breaking finance or lease, you can purchase cars for more than $30,000 — provided your investment balance is sufficient. As your income grows over time, you could increase your investment contributions to create more compounding results. The choice is yours!

After 40 years, a one million dollar investment can go on to generate millions more in income — without needing any more contributions.

We can reap huge rewards in life from a series of small, consistent, daily choices, such as how we pay for our current and future car needs.

“You only need to take a series of tiny steps, consistently, over time, to radically improve your life”

Get expert help to take action

Success with money comes down to mindset and behaviours, not intellect or luck.

At Waymaker, we provide Financial Coaching and Mortgage Broking services for everyday Aussies, helping you have finances that work.

Speak to one of our Coaches to discuss how you can avoid using debt to purchase cars and move ahead in your finances. Book a free Discovery Zoom call today:

Assumptions: 8% av. investment return annualised over 7 years. Tax and inflation not considered. All investment income is reinvested. Other assumptions apply.

Disclaimer: All information is general in nature and does not take into account your objectives, financial situation or needs. It is for education purposes only. We recommend speaking to a licensed financial advisor before many any investment or product decisions.